Stock trades, art and algorithms

If you ask me one of the more fascinating things going on out there right now is high-frequency trading. High-frequency trading (HFT) occurs when traders program computers to buy and sell stocks (or other financial products) in quick succession under certain, pre-defined circumstances. (a good starting point to learn more about HFT is this planet money episode or this ai500 article by Joe Flood).

Apparently High Frequency trading enables successful trading firms to skim of enormous surplus off these transactions (up to 1 million USD per day according to the planet money episode mentioned above). Not surprisingly this behavior can also act as a destabilizing factor wrecking havoc on stock markets. It has been one of the contributing factor’s to the ‘flash crash‘ which saw the Dow-Jones index plunge nearly 1,000 points in seconds on the 6th of may 2010.

If you believe wikipedia (which of course you should not) High Frequency trading is currently responsible for 70% of the equity trading volume in the US. Needless to say the practice is generating a fair share of controversy among economists.

At the core of this controversy are the merits of HFT: does is make macro-economic sense (because it ensures the liquidity of markets and limits market volatility) or is it detrimental to the economy at large (because it extracts value from markets based on no other fact than that prices tend to move)?

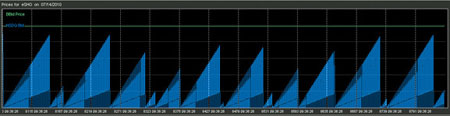

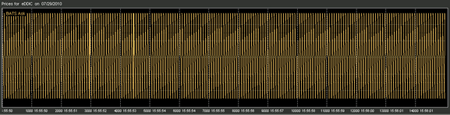

While this debate is going on it appears that there are even stranger things occurring in the field of high frequency trading: in August the Atlantic reported on research undertaken by a market data firm called Nanex that unearthed trading patterns that do not seem to make sense even by the high obfuscation standards of HFT. The article in the Atlantic claims that these strange patterns are the result of ‘mysterious and possibly nefarious trading algorithms’ whose ways and reasons of operation are known to no-one:

Unknown entities for unknown reasons are sending thousands of orders a second through the electronic stock exchanges with no intent to actually trade. Often, the buy or sell prices that they are offering are so far from the market price that there’s no way they’d ever be part of a trade. The bots sketch out odd patterns with their orders, leaving patterns in the data that are largely invisible to market participants.

When you visualize this you get something like this (graphs by Nanex):

According to the Atlantic it is unclear what exactly causes these patterns to emerge. The Nanex researchers have come to the conclusion that these algorithms are most likely an attempt by trading firms to introduce noise into the marketplace in order to realize a competitive advantage:

Other firms have to deal with that noise, but the originating entity can easily filter it out because they know what they did. Perhaps that gives them an advantage of some milliseconds. In the highly competitive and fast HFT world, where even one’s physical proximity to a stock exchange matters, market players could be looking for any advantage.

On the other hand there are much more poetic explanations for the emergence of these patterns, that abandon the idea that these patters serve a purpose all-together:

On the quantitative trading forum, Nuclear Phynance, the consensus on the patterns seemed to be that they simply just emerged. They were the result of “a dynamical system that can enter oscillatory/unstable modes of behaviour,” as one member put it. If so, what you see here really is just the afterscent of robot traders gliding through the green-on-black darkness of the financial system on their way from one real trade to another.

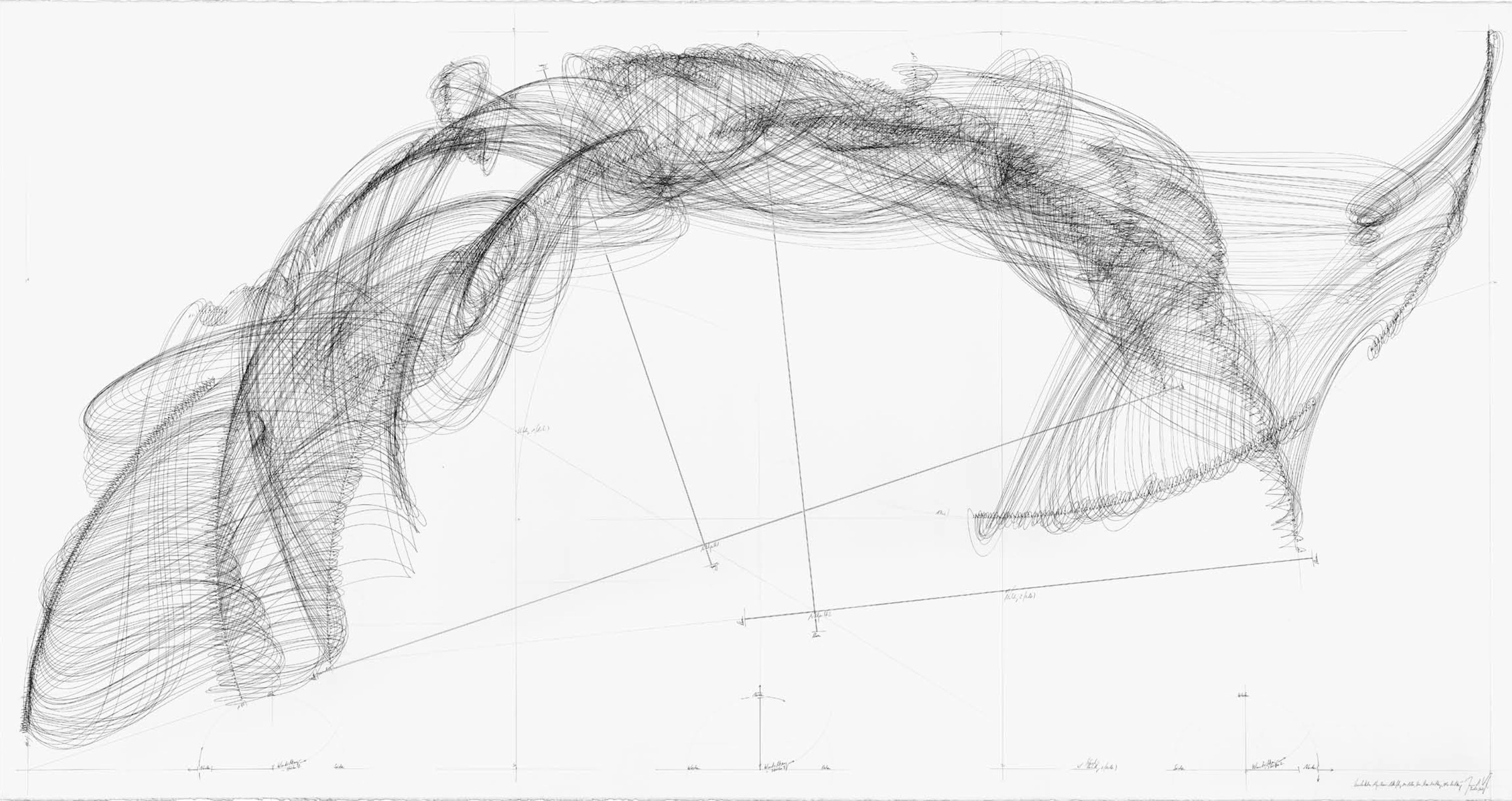

Whatever they are, these patterns are also outright beautiful. The above visualizations remind me on the work of german artist Jorinde Voigt, who’s stunning drawings (pdf) often rely on algorithms as a source:

Konstellation Algorithmus Adlerflug 100 Adler, Strom, Himmelsrichtung, Windrichtung, Windstärke -Jorinde Voigt Berlin, Oktober 2007

p.s:Sara says that these stealth trading bots remind her of the tiger in Jonathan Lethem’sChronic City instead. p.p.s: Also just finished reading ‘the Fires‘ by the aforementioned Joe Flood. brilliant book, highly reccomended.